CBDT Notification No.36/2019 Dt. 12.4.2019 – Amendment in Form 16 and Form No. 24Q under Income Tax Act

MINISTRY OF FINANCE

(Department of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

(Department of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

NOTIFICATION

New Delhi, the 12th April, 2019

G.S.R. 304(E).—In exercise of powers conferred by sections 200 and

203 read with section 295 of the Income tax Act, 1961 (43 of 1961), the

Central Board of Direct Taxes hereby makes the following rules further

to amend the Income-tax Rules, 1962, namely:—1. Short title and commencement

(1) These rules may be called the Income-tax (3rd Amendment) Rules, 2019.

(2) They shall come into force on 12th day of May, 2019.

2. In the Income-tax Rules, 1962, in Appendix II–

(A) in Form No. 16,–

(i) the “Notes” occurring after “Part A” shall be omitted;

(ii) for “Part B (Annexure), the following shall be substituted, namely:–

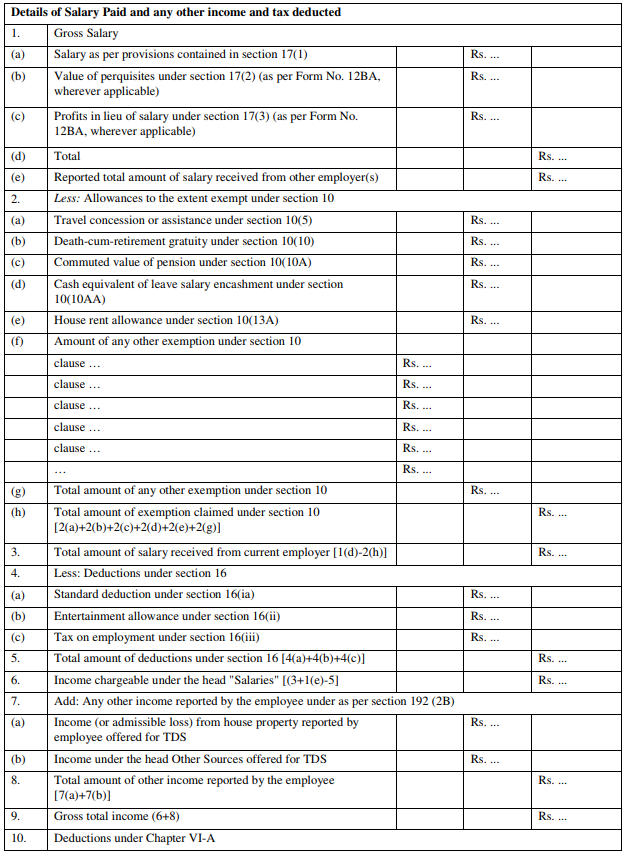

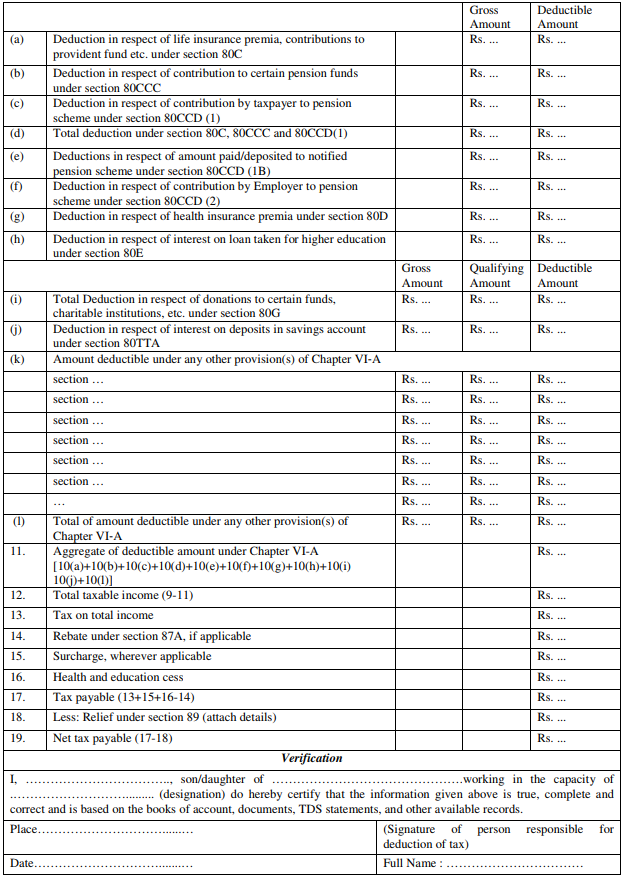

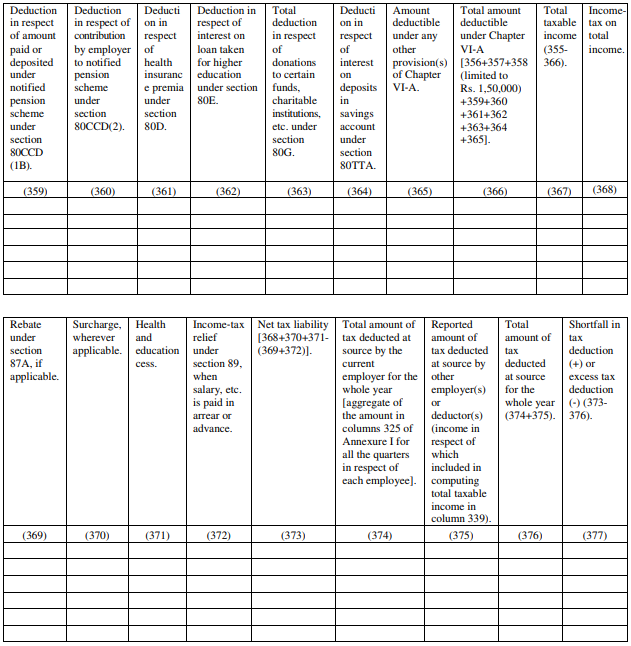

“Part B (Annexure)

Notes:

1. Government deductors to fill information in item I of Part A if tax is paid without production of an income-tax challan and in item II of Part A if tax is paid accompanied by an income-tax challan.

2. Non-Government deductors to fill information in item II of Part A.

3. The deductor shall furnish the address of the Commissioner of Income-tax (TDS) having jurisdiction as regards TDS statements of the assessee.

4. If an assessee is employed under one employer only during the year, certificate in Form No. 16 issued for the quarter ending on 31st March of the financial year shall contain the details of tax deducted and deposited for all the quarters of the financial year.

5. (i) If an assessee is employed under more than one employer during the year, each of the employers shall issue Part A of the certificate in Form No. 16 pertaining to the period for which such assessee was employed with each of the employers.

(ii) Part B (Annexure) of the certificate

in Form No.16 may be issued by each of the employers or the last

employer at the option of the assessee.

6. In Part A, in items I and II, in the column for tax deposited in

respect of deductee, furnish total amount of tax, surcharge and health

and education cess.7. Deductor shall duly fill details, where available, in item numbers 2(f) and 10(k) before furnishing of Part B (Annexure) to the employee.”;

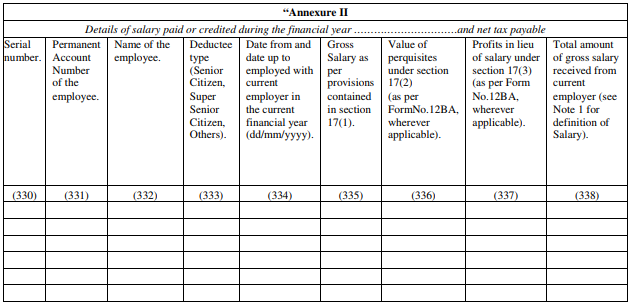

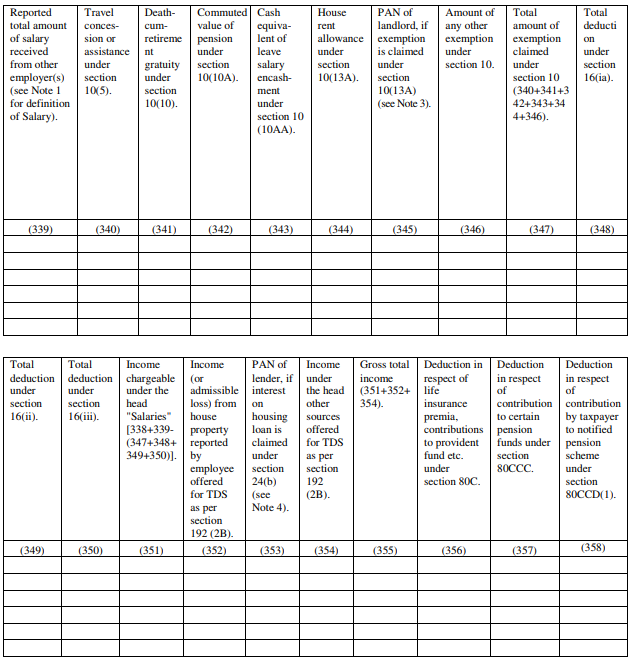

(B) in Form No. 24Q, for “Annexure II”, the following “Annexure” shall be substituted, namely:–

Notes:

1. Salary includes wages, annuity, pension, gratuity (other than exempted under section 10(10)), fees, commission, bonus, repayment of amount deposited under the Additional Emoluments (Compulsory Deposit) Act, 1974 (8 of 1974), perquisites, profits in lieu of or in addition to any salary or wages including payments made at or in connection with termination of employment, advance of salary, any payment received in respect of any period of leave not availed (other than exempted under section 10 (10AA)), any annual accretion to the balance of the account in a recognised provident fund chargeable to tax in accordance with rule 6 of Part A of the Fourth Schedule of the Income-tax Act, 1961, any sums deemed to be income received by the employee in accordance with sub‐rule (4) of rule 11 of Part A of the Fourth Schedule of the Income-tax Act, 1961, any contribution made by the Central Government to the account of the employee under a pension scheme referred to in section 80CCD or any other sums chargeable to income-tax under the head ‘Salaries’.

2. Where an employer deducts from the emoluments paid to an employee or pays on his behalf any contributions of that employee to any approved superannuation fund, all such deductions or payments should be included in the statement.

3. Permanent Account Number of landlord shall be mandatorily furnished where the aggregate rent paid during the previous year exceeds one lakh rupees.

4. Permanent Account Number of lender shall be mandatorily furnished where the housing loan, on which interest is paid, is taken from a person other than a Financial Institution or the Employer.”.

[Notification No. 36/2019/F.No. 370142/4/2019-TPL]

SAURABH GUPTA,

Under Secy. (Tax Policy and Legislation)

Note: The Principal Rules were published in the Gazette of India,

Extraordinary, Part II, Section 3, Sub-section (ii) vide notification

number S.O. 969(E) dated the 26th of March, 1962 and were last amended

vide notification number G.S.R No. 279(E) dated 01/04/2019.